WHAT WE DO

Phone:

+971 4 876 8530Email:

info@luxactuaries.com

We perform GAP analyses, financial impact assessments, transition calculations, and managed-services reserving and reporting for insurers across the Middle East and Africa.

IFRS 17 is the international standard, issued by the IASB, that governs how insurers measure and present insurance contracts. Effective from January 2023, it replaced IFRS 4 and requires insurers to measure liabilities at current fulfilment value using three models: the General Measurement Model (GMM), the Premium Allocation Approach (PAA), and the Variable Fee Approach (VFA).

The standard requires substantial changes to actuarial models, accounting systems, and data pipelines. Getting the implementation right takes specialised IFRS 17 expertise.

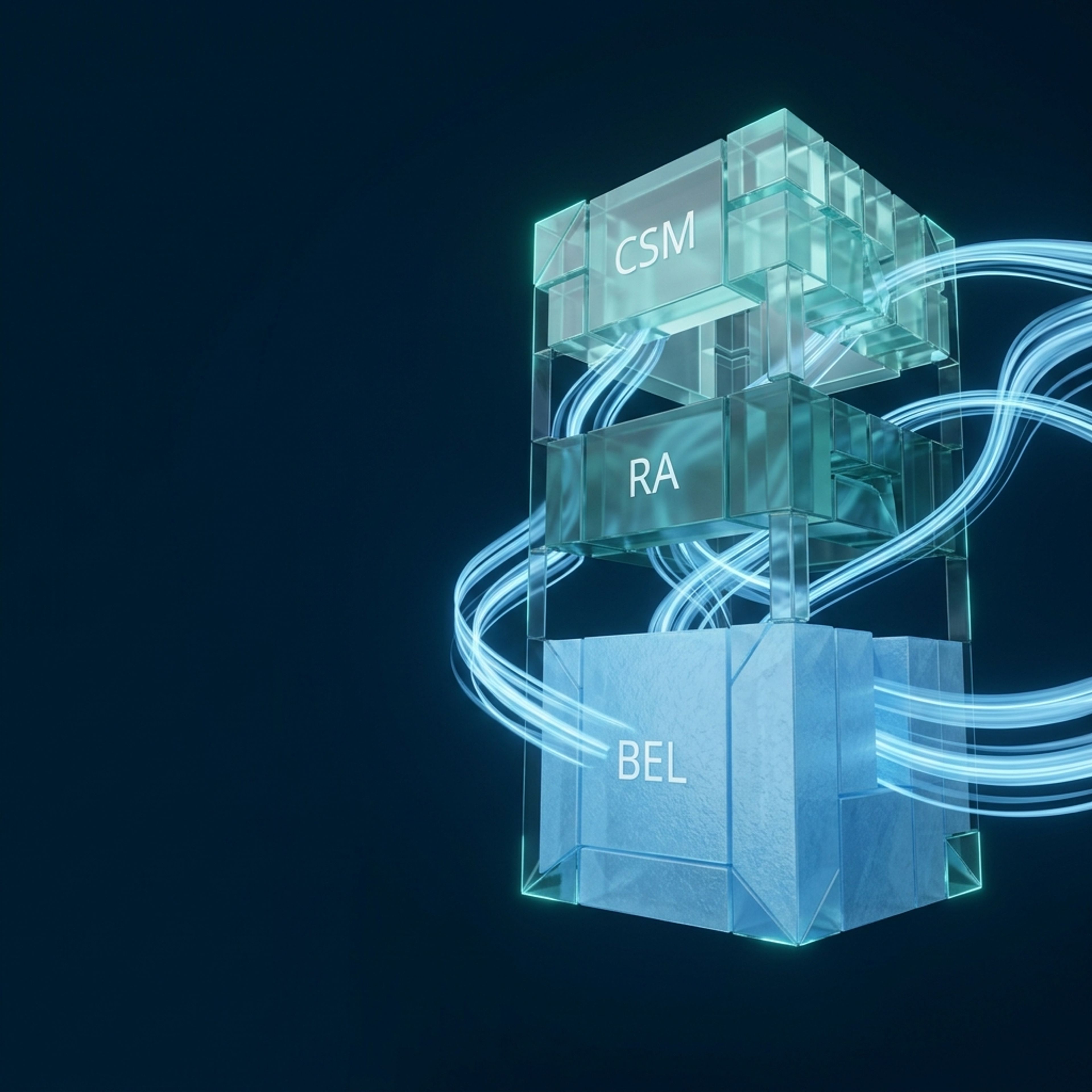

We offer outsourced IFRS 17 reserving and consulting services. Our outputs are transparent and built for auditor scrutiny, detailing the critical components of the Liability for Remaining Coverage (LFRC) and Liability for Incurred Claims (LIC).

Discuss your reporting requirements and audit timelines.

Health and Motor Insurance

Shivash BhagalooFrom scoping to audit support, we cover every stage of your IFRS 17 implementation.

We assess data, systems, and process readiness for IFRS 17 across both non-life and life portfolios.

We determine and implement the right measurement model (GMM, PAA, or VFA) and establish discount rates and risk adjustments for your portfolio.

We produce IFRS 17 disclosures including Statements of Financial Performance and Position, roll-forwards, CSM walks, and IFRS 4 to IFRS 17 equity reconciliation.

We serve insurers in the UAE, Saudi Arabia, Egypt, East Africa, and beyond, aligning local regulations with global standards.

Our experienced teams deliver accurate valuations within tight audit deadlines.

We train actuaries, finance teams, audit committees, and Boards on how to interpret the numbers, assumptions, and their forward-looking implications.

IFRS 17 needs highly granular data to group contracts into portfolios and profitability cohorts. Insurers must capture cashflows, discount rates, and risk adjustments at a much finer level than IFRS 4, which typically means upgrading actuarial systems and data pipelines.

The GMM is the default model for long-term contracts. The PAA is a simplified version, typically used for short-duration contracts under one year. The VFA applies to contracts with direct participation features, where policyholders share in the returns of underlying items.

Yes. Our team works directly with your external auditors to explain the methodologies, assumptions, and transition approaches used in our models.

Under IFRS 17, both ULAE (Unallocated Loss Adjustment Expenses) and IBNR (Incurred But Not Reported) claims are incorporated into the Liability for Incurred Claims (LIC). We model and discount these reserves using the appropriate IFRS 17 discount rate.

Get in touch for independent, audit-ready insurance contract valuations and managed services under IFRS 17.

Get in Touch Today