WHAT WE DO

Phone:

+971 4 876 8530Email:

info@luxactuaries.com

IFRS-compliant Expected Credit Loss valuations delivered by qualified actuaries. From PD/LGD models for banks to provision matrices for corporate trade receivables, we handle the technical complexity.

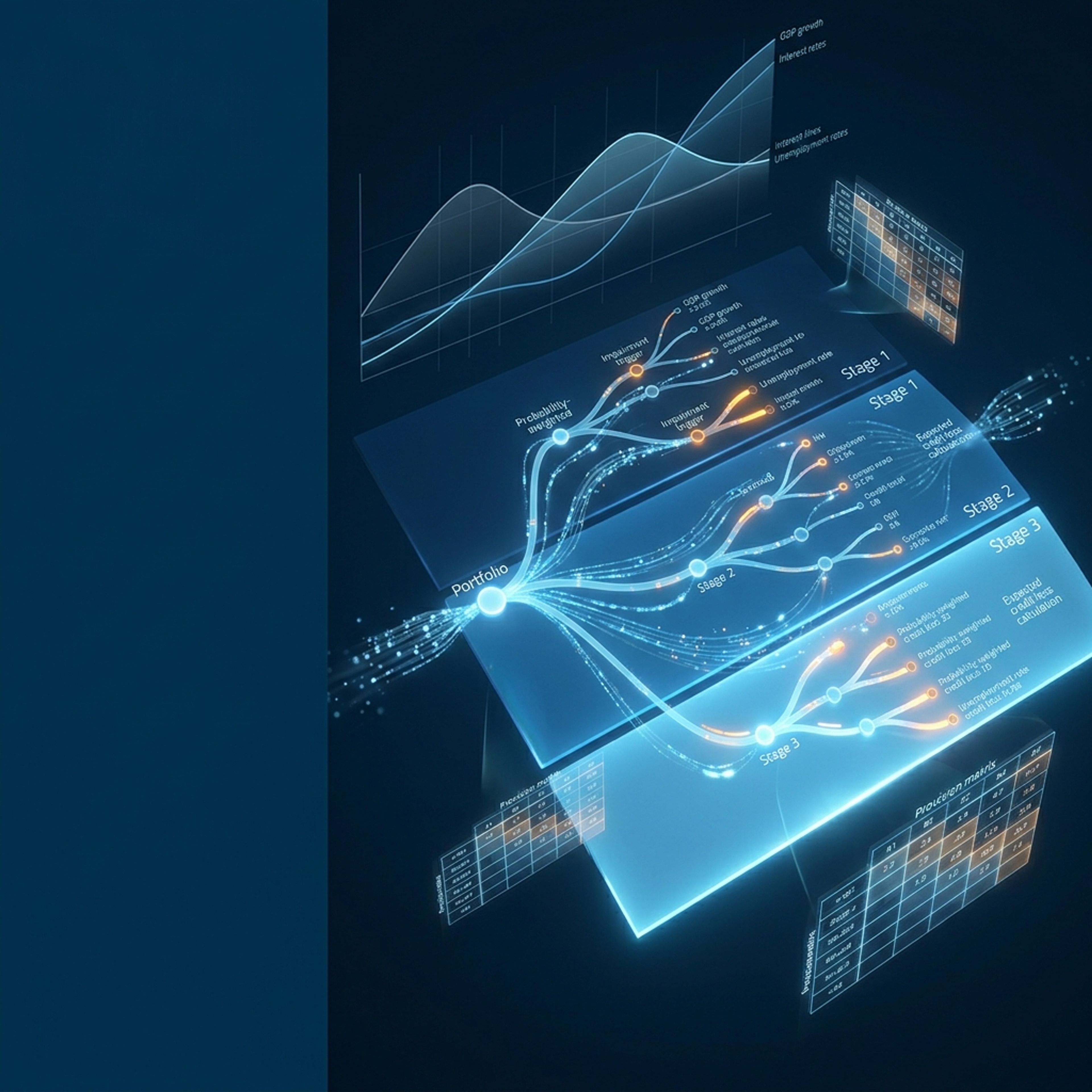

IFRS 9 requires entities to recognise expected credit losses (ECL) on financial instruments using a forward-looking impairment model. It replaced IAS 39 and requires banks and corporates to estimate credit losses before a default event occurs, using Probability of Default (PD), Loss Given Default (LGD), and Exposure at Default (EAD) parameters across a three-stage classification framework.

The shift to forward-looking ECL models requires sophisticated actuarial modelling, significant data processing, and expert judgement to get the provisioning right.

We bring specialised experience in credit risk modelling and IFRS 9 implementations, serving financial institutions across the Middle East and Africa with transparent, audit-ready ECL models and reports.

We also specialise in the IFRS 9 Simplified Approach, delivering custom provision matrices for non-financial corporates to measure lifetime expected credit losses on trade receivables.

Discuss your reporting requirements and audit timelines.

Client Manager

Ernest LouwFrom model development to audit sign-off, we handle every step of your IFRS 9 ECL provisioning.

We develop Probability of Default (PD), Loss Given Default (LGD), and Exposure at Default (EAD) models.

We integrate forward-looking macroeconomic variables and scenario weighting into ECL provisioning.

Full IFRS 9 disclosure outputs, including stage allocation and reconciliation of ECL allowances.

We serve clients in the UAE, Saudi Arabia, South Africa, and across the Middle East and Africa.

Experienced teams deliver accurate ECL valuations within tight audit deadlines.

We help your team understand the models, assumptions, and their impact on the balance sheet.

Specialised modelling for trade receivables using ageing buckets, historical loss rates, and forward-looking macroeconomic adjustments.

An ECL model estimates the credit losses an entity expects to incur over the life of a financial instrument. Unlike the old incurred-loss approach under IAS 39, IFRS 9 requires provisions before a default event actually occurs.

IFRS 9 requires ECL estimates to reflect a probability-weighted range of outcomes. This means incorporating multiple forward-looking scenarios (base, upside, downside) to adjust PD and LGD parameters.

A SICR moves an exposure from Stage 1 (12-month ECL) to Stage 2 (lifetime ECL). It is determined by comparing the risk of default at the reporting date with the risk at initial recognition, using both quantitative and qualitative indicators.

The Simplified Approach is used by corporates for trade receivables and contract assets. Instead of tracking credit risk across three stages, it requires lifetime expected credit losses to be recognised from day one.

We use a provision matrix: trade receivables are grouped by ageing bucket, historical loss rates are calculated for each bucket, and forward-looking macroeconomic overlays are applied to determine the final ECL allowance.

Get in touch for independent, audit-ready expected credit loss models under IFRS 9.

Get in Touch Today